Chinese Steel Market Highlights- Week 33, 2019

In the beginning of this week Chinese steel prices slump further amid bearish market sentiments both in domestic and overseas markets. However towards the end of this week steel prices in domestic market moved up marginally over volatile futures.

Nation’s HRC and Rebar exports offers continued to show downturn over limited trades. Meanwhile Billet export offers continued to remain downside following decline in domestic prices. Along with this raw material prices like spot iron ore prices fell and coking coal offers move down on weekly basis.

Chinese major steel producer Baosteel has announced an increase of RMB 50-150/MT for its steel products for Sep’19 deliveries.

Also National Bureau of Statistics (NBS) announced China’s crude steel output which has reduced by 3% on monthly basis to 85.22 MnT in Jul’19 over 87.53 MnT in Jun’19; amid stringent production curbs announced by provincial govt. to counter over capacity while demand remains seasonally weak.

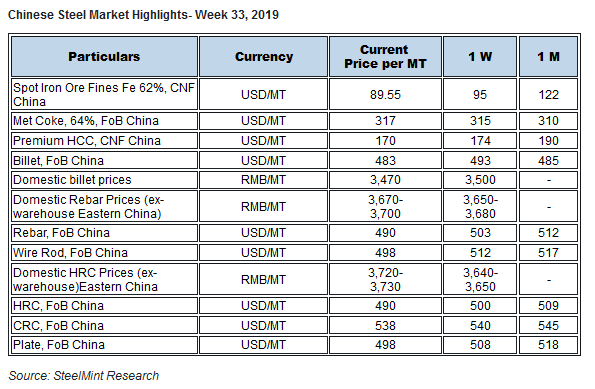

Spot iron ore prices decline further on weekly basis- Chinese spot iron ore prices opened this week at USD 88.5/MT and stood at USD 89.5/MT towards end of this week. However, on weekly basis, prices have registered a fall of USD 5/MT compared to USD 94.8/MT, CFR China towards the end of last week.

Vale during the week, announced an operation halt at its Viga concentration plant, which is part of newly acquired Ferrous Resources do Brasil (acquired on 1st Aug’19), due to permit issues, resulting in slight rise in prices during the week.

As per data compiled by SteelHome consultancy, Iron ore inventory at major Chinese ports increased to 123.15 MnT as compared to 122.5 MnT a week ago.

Spot pellet premium inched up on weekly basis- Spot pellet premium for Fe 65% grade pellets assessed at USD 27.10/MT, CFR China as against USD 26.35/MT, CFR China a week before.

Pellet inventory at major Chinese ports witnessed drop to 4.6 MnT, down on weekly basis compared to 4.9 MnT last week.

Spot lump premium fell further on weekly basis- Spot lump premium this week witnessed fall to USD 0.1550/DMTU as compared to USD 0.1600/DMTU assessed last week.

The continuous fall in lump premium has led the steel mills review cost comparison between pellet and lumps. Besides, few mills are heading towards increased usage of lumps in blast furnace replacing pellets.

Coking coal offers continue to fall further- Seaborne low-volatile hard coking coal prices continued to fall this week amid competitive offers in the Asia-Pacific markets, and lower traded prices in China.

Meanwhile in Indian market also buying interest remained thin due to the ongoing monsoon season and weakening steel prices in domestic market.

Latest offers for the Premium HCC grade are assessed at around USD 155.50/MT FoB Australia. In the beginning of the week coking coal offers were heard at USD 160.00/MT FoB basis.

China’s domestic billet prices fell on weekly basis- This week Chinese domestic billet prices in Tangshan settled at RMB 3,470/MT, down RMB 30/MT against last week. Last week domestic billet prices was hovering around RMB 3500/MT.

Chinese HRC export offers fall over mute buying- This week Chinese HRC export offers continued to slide further by around USD 10/MT as overseas buyers still assume wait and watch approach with expectation of further decline in prices.

Currently nation’s HRC export offers stood at USD 485-495/MT as against 495-505/MT FoB in previous week.

On weekly basis domestic HRC prices in China stood at RMB 3,720-3,730/MT in Eastern China (Shanghai) witnessed hike by RMB 80/MT which was RMB 3,640-3,650/MT in Eastern China (Shanghai) in previous week.

Domestic HRC prices witness slight uptick over moderate trading in domestic market. However export offers continued to weaken further.

Chinese rebar export offers continue to fall further- This week nation’s rebar export offers fell by USD 10-15/MT owing to weak end-users demand both in domestic and overseas market. Also higher inventory levels among steel mills pulled down nation’s rebar export offers on continual basis.

However overseas buyers have adopted wait and watch approach in anticipation of further fall in export offers while they have access to cheaper products from other regions.

On an average basis currently nation’s rebar export offers stood at USD 485-495/MT FoB China which was around USD 500-505/MT FoB basis last week.

Meanwhile domestic rebar prices stood at RMB 3,670-3,700/MT (Eastern China) registered an increase by RMB 20/MT against RMB 3,650-3,680/MT (Eastern China) a week ago.

source: SteelMint

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution