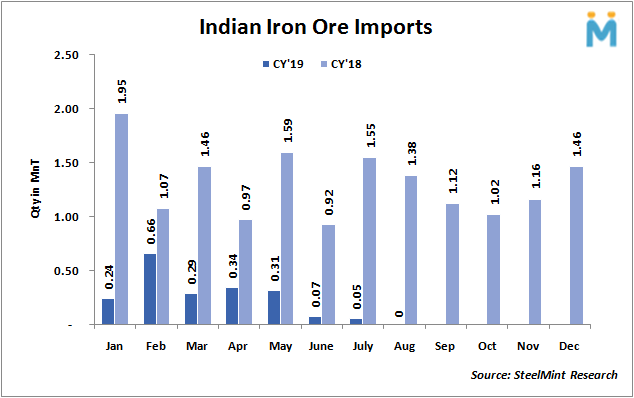

Indian Iron Ore Imports Recorded Nil in Aug'19 Over Competitive Domestic Prices

Indian iron ore imports for the month of Aug’19 have been recorded nil, according to the data maintained by SteelMint. The imports have dropped to nil after 4 years as this level was last witnessed in Oct’15. Indian iron ore imports in July’19 stood at 51,470 MT.

Though the spot iron ore fines (Fe 62%) decreased sharply by 23% in Aug’19, it is still non-viable to import iron ore on falling domestic sponge and semi-finished steel prices. Monthly average iron ore prices stood at USD 92/MT, CFR China in Aug against previous month at USD 120/MT, CFR China amid sluggish demand and increased iron ore inventory at Chinese port.

Why have Indian iron ore imports dropped in Aug’19?

1. Competitive domestic iron ore prices:

Indian domestic prices witnessed fall for the month. NMDC reduced iron ore fines and lump prices by INR 200/MT last month in both Chhattisgarh & Karnataka, and DRCLO prices by INR 230/MT. Odisha iron ore miners are yet to announce price revision however market participants expect price correction on falling sponge and semi-finished steel prices. However lower production amid monsoon remains a concern.

2. Softening domestic steel prices:

Limited trades and weak demand along with low buying sentiments in the finished steel prices lead to continual fall in steel prices. Domestic HRC prices in Indian trade segment fell by INR 500-1000/MT in last one month.

3. Domestic pellet preference over imported South African lumps:

Imported South African lumps inquiries in India continued to remain slow as the domestic pellet was more preferable. West India based steel mills preferred domestic pellets. SteelMint's assessment for South African lump was recorded at USD 120/MT, CFR India towards end of Aug, down by USD 15 against last month.

source: SteelMint

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution