Iron ore offers little support to scrap price in Europe

Iron ore prices have surged since April, but this has had little impact on European ferrous scrap prices and is likely to provide only limited support in the coming two to three months.

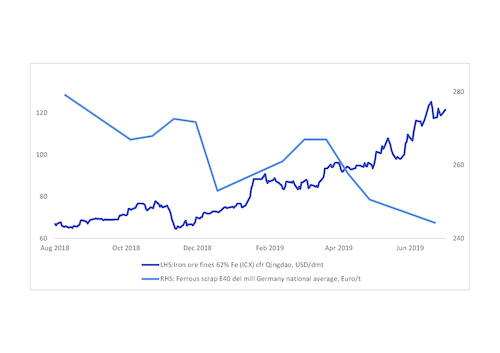

The Argus daily 62pc Fe iron ore fines cfr Qingdao (ICX) assessment rose to $121.35/t on 15 July from below $90/t on 2 April because of expectations of tighter supply from major iron ore suppliers and limited intent from Chinese steel mills to reduce output, despite falling margins.

Some European market participants previously anticipated that the increase in iron ore prices in China, which is the main driver of European iron ore prices, would support European delivered to mill ferrous scrap prices in June and July. The expectation was that blast furnace-based steel mills might increase their use of scrap to offset higher iron ore costs.

European blast furnace mills typically consume a mixture of iron ore pellets and fines that they purchase through long-term contracts. Prices under the contracts are usually linked to one or a basket of cfr China indexes.

But scrap demand from many northwest European mills since April has fallen or remained largely unchanged at best. Weaker steel demand and prices coupled with scheduled maintenance and upgrade works at steel mills were the main drivers behind the fall in scrap demand.

The Argus monthly national average assessment for E40 shredded ferrous scrap delivered to mill in Germany fell to €239.26-249.26/t in July from €262-272/t in April.

Many mills were also unable to significantly increase the percentage of scrap used in blast furnaces because of technical reasons.

"It is not that easy to increase scrap usage in blast furnaces. Most mills in Europe have probably reached the maximum charge rate of scrap and will not be able, or even consider, to use more scrap even if iron ore prices rose above $200/t," one European steel mill said.

Another steel market participant noted that some US mini-mills have been looking at options to displace some direct reduced (DR) pellets with high-grade scrap products, but added that this activity is fairly limited within Europe.

The average scrap utilisation rate in European blast furnace crude steel production is around 15-20pc, according to estimates by multiple steelmakers.

The availability of competitively priced pig iron further dented some European mills' appetite to use more scrap. Scrap demand from some integrated mills in northwest Germany was lower in June and July as prices for contracted pig iron were considerably cheaper than scrap, one scrap supplier said.

Pig iron prices in Europe were also under pressure in May-June. The Argus assessment for Russian/Ukraine basic pig iron, two of the main suppliers of European imported pig iron, fell to $334/t fob Black sea on 27 June from $350/t on 25 April. Prices rebounded to above $340/t fob in mid-July because of reduced availability and higher sales to the US. But spot demand from European mills was still comparatively weak, market participants said.

Logistical price boost

Market participants expect scrap prices in Europe to have little support in the next two to three months as steel demand and prices are unlikely to rise, while Turkish demand for imported scrap will be volatile depending on Turkish mills' ability to export steel products.

But scrap prices could increase in the event of even a minor disruption to availability, particularly because flows are relatively tight as a result of slower manufacturing activity in the past few months and a seasonal fall in collection rates over the next six to eight weeks.

Any major disruption to scrap transportation through the inland waterway system in Germany, Belgium and the Netherlands may significantly reduce scrap suppliers' ability to efficiently allocate material between domestic and export markets. This may create a shortage of scrap and lift prices in some regions, as happened last summer.

German domestic scrap delivered to mill prices in August 2018 were limited to a fall of around €5/t from the previous month compared with initial expectations of a minimum €10/t drop, as suppliers were unable to move material on the Rhine river from southern Germany.

Exports from Belgium, Germany and the Netherlands, including trades between these countries, totalled 4.5mn t in August-October 2018, down by 4pc from over 4.7mn t in the same period a year earlier.

Water levels on the Rhine at the key measuring point of Kaub near Frankfurt fell below the loading threshold for some cargoes and vessels on 15 July for the first time this summer and have since remained below the threshold. Water levels are expected to continue to fall this week, which will further increase loading restrictions.

Some scrap suppliers said they do not expect the disruption to be as bad as last year because they have had more rainfall so far this year. But monitoring service Elwis forecasts only one day of rainfall in southwest Germany and Switzerland for the remainder of this month.

Transportation of scrap on trains to some destinations in northwest Europe is an alternative. But the problem of limited-to-no availability of cargo wagons in Germany that affected scrap mobility in 2018 remains unsolved, some scrap suppliers said.

China iron ore 62pc Fe vs Europe ferrous scrap E40 shred

source: Argus Media

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution

Zahit Aluminium confirms performance of Danieli Breda extrusion press in Turkey

Henan Jiyuan Iron & Steel awards Danieli for new Jumbo Rounds caster in China

Danieli Seven-Life Side Guides successfully commissioned at Hoa Phat Dung Quat on QSP® line