Chinese Steel Market Highlights - Week 13, 2019

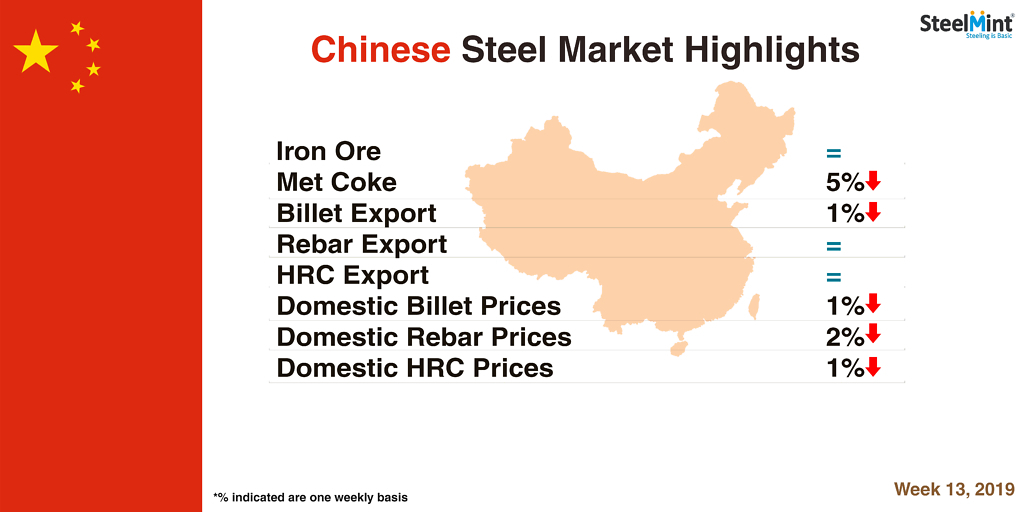

This week Chinese steel prices reported decline over weak trading in domestic market and fluctuating futures. Country’s rebar and HRC export offers remained stable this week. Coking coal offers moved down this week over limited trades from China. However iron ore prices recorded increase towards the weekend.

Chinese mills announced increase in ferro chrome tender price for Apr’19.

Coking coal prices moved down this week- Seaborne coking coal prices fell since last two weeks as most of buyers in China refrained from actively procuring imported cargoes over the expectations of a weakening market sentiments ahead.

Thus coking coal supply levels remain sufficient to outweigh the limited demand appetite, which has exerted a lot of pressure on May and June forward-loading cargoes.

Thus, latest offers for the Premium HCC grade are assessed at around USD 207/MT FOB Australia which was reported USD 212/MT FoB basis last week.

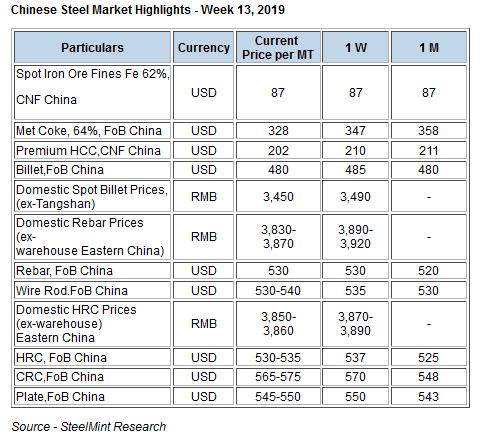

Chinese spot iron ore prices rise towards weekend - Chinese spot iron ore prices opened up this week at USD 84.95/MT,CFR China and increased to USD 87.05/MT towards the weekend amidst drop in Vale (world’s largest iron ore miner) sales estimate for 2019.

Vale decreased its sales estimate for 2019 between 307 MnT and 332 MnT.This is lower by 75 MnT against its previous estimated forecast.

Iron ore inventory at major Chinese ports have decreased to 147.6 MnT this week as against 148.6 MnT a week ago.

Spot lump premium witnessed drop to USD 0.3285/MT,CFR China as against USD 0.3465/DMTU a week ago amid availability of cheaper substitutes since steel mills were replacing lumps with pellets. Also, the expectation of end to sintering cuts has put pressure on lumps.

Spot pellet premium up by USD 1.25/MT this week -: Spot pellet premium for Fe 65% grade pellets have increased to USD 33.55/MT, CFR China this week, against USD 32.30/DMT a week before.The increase is attributed to rise in pellet preference in China.However, pellet inventory at major Chinese port increased to 5.25 MnT this week compared to 5.2 MnT last week.

Chinese domestic billet prices fall - Domestic spot billet prices in China’s Tangshan closed this week at RMB 3,450/MT (ex-works, including VAT) against last week’s assessment of USD 3,490/MT (ex-works, including VAT).

Chinese HRC export prices remain stable this week - Nation’s HRC export offers remained stable this week as the prices remained firm in domestic market.

Currently nation’s HRC export offers is assessed at around USD 530-535/MT FoB basis. Last week the prices continued to remain at similar levels.

However buyers in Vietnam are bidding on lower side owing to soft demand in downstream products.

On weekly basis domestic prices in eastern China (Shanghai) decline by RMB 20/MT and stood at RMB 3,850-3,860/MT.

Chinese rebar export offers remained firm this week- This week rebar export offers remained unchanged over weak buying.

Currently,nation’s rebar export offers are at USD 530/MT FoB China. Last week also the offers remained at similar levels.

Meanwhile domestic rebar prices decline by RMB 60/MT on W-o-W basis and is assessed at RMB 3,830-3,870/MT in (Eastern China).

Last week the prices stood at RMB 3,890-3,920/MT inclusive of VAT taxes.Thus increase in rebar output lead to decline in prices in domestic market.

source: SteelMint

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution

Henan Jiyuan Iron & Steel awards Danieli for new Jumbo Rounds caster in China