Will Indian Long Steel Prices Decline Further ?

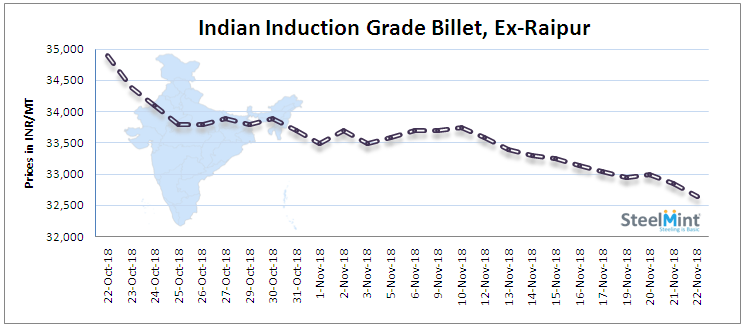

Iron & Steel prices in Indian domestic market have been falling since the beginning of November'18 due to poor off take in finished steel products, healthier supply, lessened exports & improved import parity.

The Semis manufacturers are forced to cut prices even though the margins (conversion spread) are limited. Similar comments were received from re-rollers as capital of the producers is stuck due to rising stock in the mills.

As per assessment in last couple of weeks, the domestic price fall is about INR 500-1,500/MT (USD 7-21) in Semis & Secondary Finished long steel products.

However during the tenure, prices of key raw material such as iron ore, pellet & coal declined marginally by INR 500-700/MT (USD 7-10).

Thus, the cost of productions with standalone mills are more or less firm on limited corrections in raw materials. However as the prices of final products slump, the margins (conversion spread) dipped to bottom line.

On an average the sponge producers in Central & East India are getting conversion is about INR 14,000/MT or USD 198 (from Pellet to P-DRI).

While standalone Billet mills are getting conversion of about INR 12,000/MT or USD 170 (from P-DRI to Billet), while re-rollers are fetching close to INR 3,500-4,000/MT (USD 50-57) conversion from Billet to 12mm rebar.

As per manufacturers the mentioned conversions are not up to the mark (lessened than the required). If the prices fall further, they might curtail productions, which is likely to balance the supply-demand and indirectly support declining prices.

source: SteelMint

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution