Global copper output up 7.1 pct in first three months of 2018

Miners around the globe dug up 330,000 more tonnes of copper between January and March this year than in the same period of 2017, helped by higher production in world’s leader Chile, data released by the International Copper Study Group (ICSG) shows.

The general increase, a 7.1% compared to Q1 2016, was mirrored by both concentrates (+7%) and solvent extraction-electrowinning or SX-EW (+7.3%) production.

Output in Chile increased by 19% mainly because production in February/March 2017 was constrained by a strike at Escondida, the world’s biggest copper mine, but also due to an improvement in state-owned miner Codelco’s production levels.

Miners around the globe dug up 330,000 more tonnes of copper between January and March this year than in the same period of 2017.

Indonesian output rose by 58% because comparative output in 2017 was negatively affected by a temporary ban on concentrate exports that started in January and ended in April.

A 9.5% increase in SX-EW production in the Democratic Republic of Congo (DRC) and a 16% rise in Zambian mine output due to the restart of temporarily closed capacity.

Although there were no major supply disruptions in the period, overall growth was partially offset by lower output at some mines in Canada (-10%) and in the U.S. (-7.5%), the ICSG says.

After a strong increase in the last few years due to new and expanded capacity, output in Peru (the world’s No.2 copper mine producing country) has levelled off.

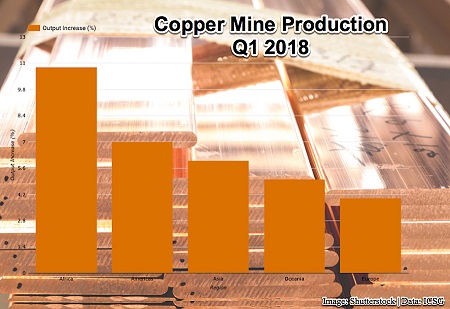

On a regional basis, mine production is estimated to have increased by around 11% in Africa, 7% in the Americas, 6% in Asia, 4% in Europe and 5% in Oceania.

According to the ICSG, global refined copper output increased 3% in the first quarter of the year when compared with Q1 2017, with direct use scrap output growth (+6%) outpacing primary production (+2.3%) on a year over year basis.

Apparent usage was estimated to have increased 1.8% y/y in Q1 with consumption growth in China driven by a significant increase in refined copper imports, up 10% y/y. Analysts at BMO Metals, however, believe inventories in China increased at the lowest pace in recent history over that period.

source: Mining.com

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution

Henan Jiyuan Iron & Steel awards Danieli for new Jumbo Rounds caster in China