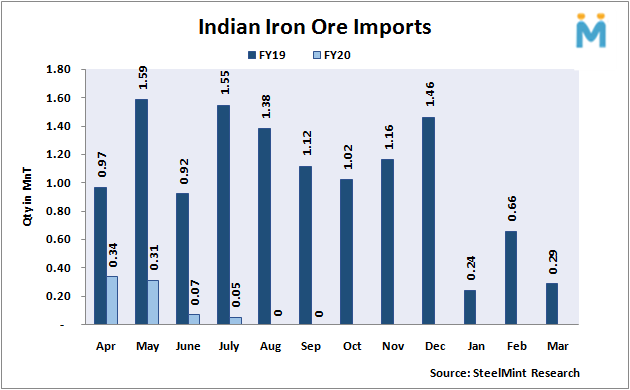

Indian Iron Ore Imports Continue to Remain Nil in Sep’19

Indian iron ore imports were reported nil in Sept'19, according to the data maintained by SteelMint. The imports have recorded nil for second consecutive month. Indian iron ore imports in July’19 stood at 51,470 MT.

Monthly average iron ore prices stood at USD 93/MT, CFR China in Sep against previous month at USD 92/MT, CFR China. Although the spot iron ore fines (Fe 62%) index witnessed drop in past few months against USD 120/MT, CFR China assessed towards July’19. However, it is still non-viable to import iron ore on falling domestic sponge and semi-finished steel prices.

Why have Indian iron ore imports recorded nil for the month?

1. Competitive domestic iron ore prices:

Indian domestic miners slashed prices in Sep’19. NMDC reduced iron ore lumps and fines prices by INR 200/MT and DRCLO INR by 230/MT from Chhattisgarh mines, and from Karnataka mines reduced prices INR 300/MT in both fines and lumps. Also, major Odisha miners increased discount for bulk iron ore fines booking and Serajuddin mines reduced lump offers by INR 300/MT.

2. Domestic pellet preference over imported South African lumps:

Imported South African lumps inquiries in India continued to remain slow last month as the domestic pellet was more preferable. West India based steel mills preferred domestic pellets.

SteelMint's assessment for South African lump witnessed at around USD 103-105/MT, CFR India towards end of Sep against USD 120/MT, CFR China towards end of Aug’19. However, the prices are still unviable for purchases. Domestic pellet offers of Jindal SAW for Fe 63% grade were assessed at INR 8,050/MT del Kandla in end Sept'19 against INR 7,500/MT a month ago.

source: SteelMint

Top News