Chinese steel export threat looms over scrap markets

The relative strength of China's steel markets has frozen its spot export sales, easing the glut in seaborne trade, but some Asian scrap market participants are not sure how long that absence will last, especially as China's slower winter demand season takes hold.

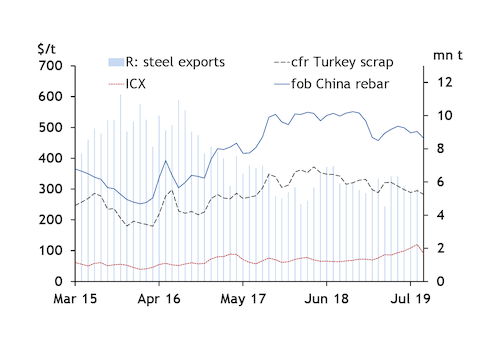

Most steel products in China are priced higher than seaborne levels, keeping its supply at home and even turning interest to steel imports to China. That price strength sent China's steel exports to a six-month low in August, down by 15pc on the year, with year-to-date exports down by 4.4pc to 44.97mn t.

But at the same time, China is the world's fastest-growing steel producer, with crude steel output on pace to reach nearly 1bn t in 2019, under a 9.1pc growth rate through August national bureau of statistics data show.

China is expected to impose flexible output restrictions during its November-March winter season, a time when construction demand slows and steel inventories soar to annual peaks in February-March. The looser restrictions and slowdown in sales, as well as intact profit margins keeping supply on line, could send China's steel markets into oversupply.

When China's domestic markets are oversupplied, exports are its only course of action. The last time China pivoted back to exports, it put enormous pressure on prices for steel and its raw materials.

When China's steel exports surged by 24pc to a record 110mn t in 2015, global ferrous prices plunged to multi-year lows.

The Argus HMS 1/2 80:20 scrap cfr Turkey assessment fell to a five-year low of $170/t cfr in October 2015. Two months later, the Argus ICX 62pc iron ore fines index fell to an all-time low of $37.30/dry metric tonnes (dmt) cfr Qingdao, and the fob China rebar price fell to $247.50/t fob.

By comparison, today the fob China rebar price is $432/t, 75pc higher than the 2015 low, and the Argus ICX is at $92.90/dmt, 149pc higher than 2015. But Turkish scrap at $235/t yesterday was only 38pc higher than the 2015 low, reflecting the extent to which the scrap market has fallen sharply over the past two months despite a relative firmness to Chinese pricing.

Seaborne ferrous scrap markets will crash if China starts to export more steel, a major scrap trader in northern Asia said.

Asia-Pacific ferrous scrap markets are already facing pressure from increased supply of semi-finished steel at lower prices.

Taiwan's domestic market rebar prices were at 14,400-14,500 New Taiwan dollars/t ex-factory ($468-471/t) this week, while local billet was priced at NT13,000/t ($422/t) delivered to customers and imported billet prices were heard to be around $400/t cfr Taiwan.

With the current import of overseas billet, Taiwanese mills face stiff competition for rebar sales with domestic re-rollers, which is the reason why mills are trying hard to keep scrap prices low.

A scrap-based mill has costs of around $160/t to turn imported scrap into steel. With Taiwanese containerised scrap import costs at $223/t cfr Taiwan, that is close to re-rollers' costs of roughly $400/t to make rebar.

If China or other regions export more semi-finished steel to Taiwan, its local mills that do not use imported billet will have to further cut costs and prices.

China's mills have been aggressive in export markets whenever they have firmly turned their attention overseas. Chinese domestic profit margins remain intact and could subsidise less profitable export sales, unlike in 2015 when its mill margins turned negative.

But China has fewer options for overseas exports than in 2015-16, as many countries have since added more trade protection measures, which means that competition could be even more fierce in the Asian markets that are still viable targets.

source: Argus Media

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution