Indian Steel Market Weekly Snapshot

Indian steel prices remained volatile during the week 26 (22nd to 29th Jun) as domestic trades were not up to the mark for Semis & Finished products amid rising inventories with the mid sized mills, as reported by industry participants.

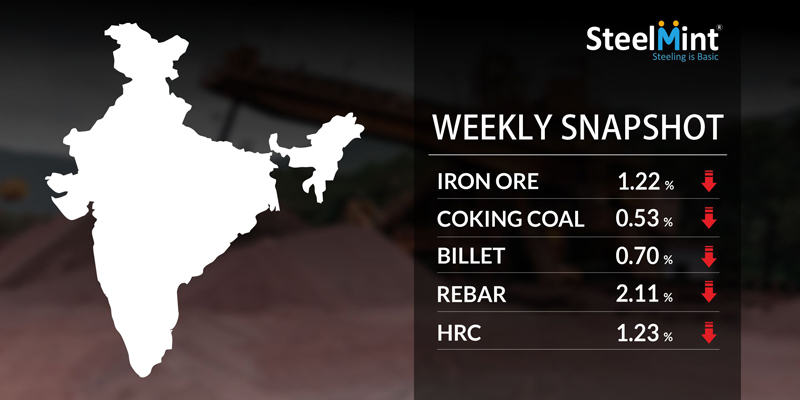

As per assessment, this week prices of Semis products volatile by INR 100-500/MT. However Finished Long & Flat steel prices dropped by INR 500-1,000/MT (USD 7-14) across regions on account of limited inquiries, which in turn piled up stock.

IRON ORE & PELLETS

NMDC Ltd- India's biggest iron ore producer has announced a roll over in its iron ore prices for July deliveries yesterday. Odisha merchant miners also kept iron ore prices unchanged for this week.

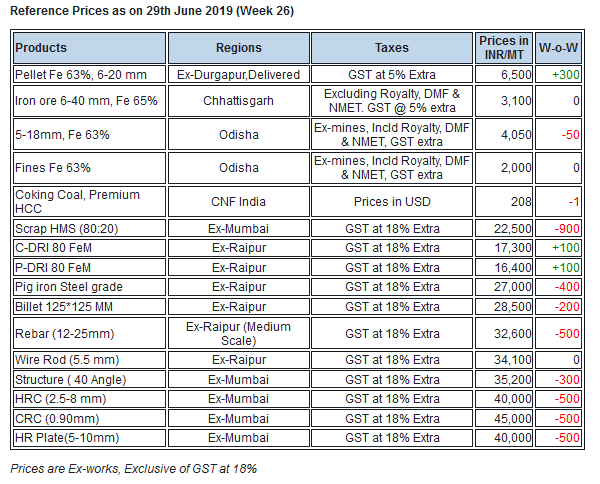

Majority of central & eastern India based pellet makers are eyeing export markets amid high realisation. Durgapur (eastern India) based pellet makers have raised offers following hike in export offers. SteelMint’s reference pellet price assessment stands at INR 6,500/MT (delivered) up by INR 200-300/MT against INR 6,200-6,300/MT last week. Central India (Ex-Raipur) offers at INR 6, 800/MT. Preference to iron ore lump has softened demand for pellets.

-- India's KIOCL signs MoU with Glencore & Steel Mont for pellet supply of around 400,000 MT to European markets including UK.

-- KIOCL concludes 50,000 MT domestic Iron ore concentrate (Fe 63.5%) purchase tender at around INR 6,050/MT CFR Mangalore port. The due date was on 14th June’19.

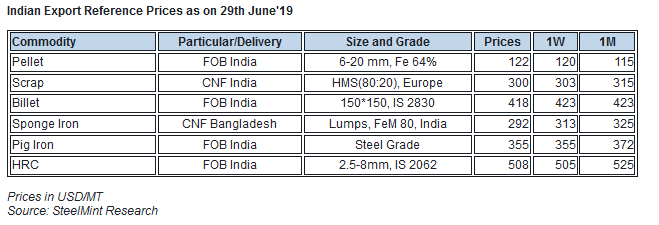

-- Central India based pellet maker concludes 50,000 MT export deal to China USD 130/MT CFR. Another deal reported by east India based pellet maker for standard grade pellets at USD 133-134/MT, CFR China.

-- As per WSA (World Steel Association) India’s crude steel output moved up by 5% to 9.19 MnT in May’19 against 8.78 MnT in the preceding month.

COAL

Australian coking coal export prices have slide further amid weakening global demand in response to the bearish outlook in major steel-producing countries.

In China, seaborne coking coal of high coke strength after reaction, low ash and sulphur properties have been a price competitive option, relative to domestic coking coal of similar specifications, but end-users continue to adopt a cautionary stance towards procurement.

In Australia, the spot supply of hard coking coal is tighter compared to premium low-volatile cargoes. This shortage should ease the fall in prices of hard coking coal with low ash and sulphur.

-- In the Indian market, trading activities remained thin without any immediate spot demand due to the timely onset of monsoon season. Latest offers for the Premium HCC grade are assessed at around USD 195.00/MT FOB Australia and USD 207.60/MT CNF India.

-- MMTC, India’s largest and state-owned trading house, issued a tender for the sale of 15,000 MT coking coal. The due date for submitting the bids is 02 July’19.

SCRAP

Indian imported scrap market remained almost quiet with very limited trades reported this week. The market is expecting for a recovery next week with the recent rebound in Turkey prices although prices stand range-bound after hitting the bottom. Concerns on US-China meet, lack of clarity on budget, weakened domestic steel prices and the arrival of monsoon kept sentiments non-viable for scrap imports.

-- SteelMint’s assessment for containerised Shredded from Europe, UK and US slightly improve to USD 315-318/MT, CFR Nhava Sheva. However, no major deal reported in the market.

-- Few trades for low priced scrap were reported in the opening of the week. UK origin Turning scrap sold at USD 265-270/MT, CFR and HMS offers stood in the range of USD 300/MT, CFR. South African HMS 1&2 was reported at around USD 315/MT, CFR. On improved domestic demand Dubai based scrap sellers remain mostly away from offering much with HMS 1&2 assessment at around USD 310/MT, CFR. West Africa HMS at around USD 290-295/MT, CFR.

SEMI FINISHED

Indian Semi finished steel market observed volatility in prices due to fluctuating demand and during the week Sponge iron offers surged in Central & Eastern regions by INR 300-500/MT (USD 4-7), however downfall seen in Southern India by INR 500/MT.

In line domestic billet market also marked mix trend, where prices volatile by INR 100-500/MT, W-o-W.

-- Indian steel export offers to Nepal dropped, however trade volumes improved as per participants and deals reported for Billet (induction grade, 100*100 mm) at USD 400-405/MT & for Wire rod (commercial grade, 5.5 mm) at USD 470-475/MT ex-mill, Durgapur. Freight cost to Nepal is about USD 25-30/MT.

-- Indian Sponge iron export offers drop further and latest assessment stood at around USD 280/MT CPT Benapole(dry port of India & Bangladesh), equivalent to USD 295/MT CNF Chittagong, Bangladesh.

-- RINL has invited a tender for export of 30,000 MT Billets and 20,000 MT Bloom. The due date for bid submission is 2nd Jul’19. The company also floated export tender for Nepal of 10,836 MT Billets and 5,418 MT Wire Rod, which due date for bid submission is 2nd Jul'19.

-- SAIL has invited an ocean export tender for 16,200 MT Prime Mild Steel Non-Alloy Concast billets (150*150 mm) from Durgapur Steel plant. The last date for bid submission is 28 Jun’19.

-- Rashtriya Ispat Nigam Limited (RINL)- state-owned steel maker under the Ministry of Steel, has invited a tender for export to Nepal . The due date for bid submission is 02 Jul’19 till 15:00 hrs

-- TATA Metaliks Limited (TML) - known as the largest foundry grade pig iron manufacturer in eastern India has reduced foundry pig iron prices by INR 800/MT (USD 12) to INR 31,700/MT (USD 457), ex-plant, Kharagpur, eastern India.

-- Jindal Steel has further cuts price and reported steel grade pig iron at INR 26,500-26,700/MT ex-Raigarh & panther shots (granulated pig iron) at INR 24,500-24,700/MT ex-Angul, Odisha.

-- SAIL’s Rourkela Steel Plant tender held on 24th Jun'19 to sell about 3,800 MT steel grade pig iron has received weak response. The base price for the tender was quoted by RSP at INR 27,250/MT and near about 85% material unsold. Further the plant has schedule an auction to sale 3,400 MT basic grade Pig iron whose due date is 29th Jun'19.

FINISH LONG

Indian Finish Long steel market have been observed limited demand amid dull sentiments across regions, hence price range down by INR 500-1,000/MT, in which major fall of around INR 1,000/MT registered in Jalna (Maharashtra) due to mounting stock with the mid scale mills.

Moreover participants believe that, Indian finish long steel prices to range bound till the National budget declaration which is scheduled on 5th Jul'19. Although inventories being stated slightly high in comparison to average levels particularly in Western and Central India.

-- Current trade reference rebar prices (12-25 mm) assessed at INR 32,500-32,700/MT Ex- Raipur & INR 33,400-33,700/MT Ex-Jalna; prices are basic & excluding 18% GST.

Further this week, State owned large mills have maintained finish long steel prices and current trade reference rebar (12 mm) price registered at INR 39,500-40,000/MT Ex-Chennai (Stock Yard) and Structure (Channel 125) registered at INR 40,400/MT Ex-Mumbai (Stock Yard).

-- Central region, Raipur based heavy structure manufacturers have slightly raised trade discount by INR 100-200/MT to INR 800-1,000/MT against last week and trade reference prices stood at INR 36,900-37,300/MT (200 Angle) ex-work.

-- Trade discounts in Raipur Wire rod firm this week at INR 1,000-1,200/MT. The fresh trade reference prices hovering at INR 33,000-33,700/MT ex-Durgapur & INR 33,500-34,100/MT ex-Raipur, size 5.5 mm.

-- Anti-dumping duty on imports of Ductile Iron (DI) pipes further extended till 9th Oct'19, as per recent notification by Indian government.

FLAT STEEL

Domestic HRC prices in traders market have come down further by INR 500-1,000/MT against last week and are hovering at almost 4-months low. Similar levels were recorded in the month of Feb’19.

Currently, HRC (2.5-8 mm, IS2062) trade reference price is around INR 40,000/MT ex-Mumbai, INR 40,000-40,500/MT ex-Delhi and INR 42,000-42,500/MT ex-Chennai. The CRC (0.9 mm, IS 513) trade reference price is around INR 45,000/MT ex-Mumbai, INR 43,250-45,000/MT ex-Delhi and INR 46,000-47,000/MT ex-Chennai. Prices mentioned above are basic and extra GST@ 18% will be applicable.

Thus slowdown in auto sector and construction activities amid delayed funding from government has resulted to slump in demand in domestic market. Meanwhile cheaper imports arriving from Japan and Korea under Free Trade Agreement (FTA) resulted to domestic HRC prices under pressure.

source: SteelMint

Related News

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution

Henan Jiyuan Iron & Steel awards Danieli for new Jumbo Rounds caster in China