Indian Steel Market Weekly Snapshot

During the week-22 (25th May to 1st Jun'19), Indian domestic trade activities were subdued. The mid size mills reported mix response from the domestic buyers over uncertainty in the market. Meanwhile strong supply has push prices on downtrend.

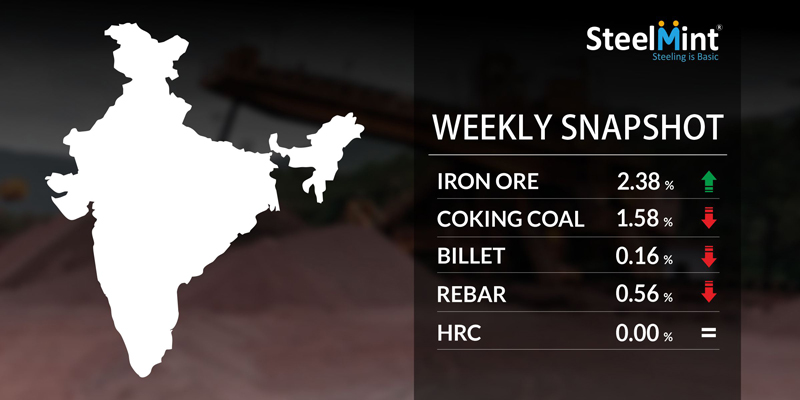

As per SteelMint's assessment, in these days the prices of Semis & Finished Long steel products fell by INR 100-500/MT (upto USD 7). In context to Flat steel, the prices have remained firm through the traders end.

However in conversation with participants SteelMint learned that, the large mills are planning to hike finished steel prices by INR 500-1,000/MT (USD 7-14) for June deliveries on account of higher raw materials.

IRON ORE and PELLETS

National Mineral Development Corporation (NMDC) has announced an increase in floor prices for upcoming Karnataka e-auctions by around INR 250/MT (USD 3.6) for both fines and Lumps. Few of the major Odisha based major merchant miners including Rungta Mines, Serajuddin, RP Sao, KJS Ahluwalia and Kaypee Enterprises have raised iron ore offers INR 300/MT in lumps and INR 200/MT in fines.

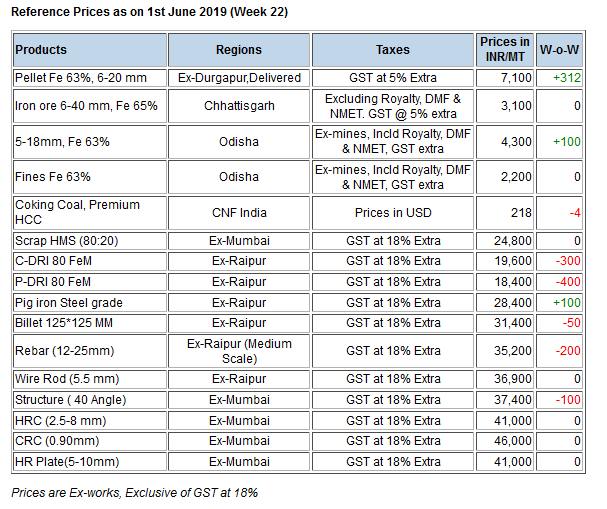

India domestic pellet prices increased amid trades have turned dull with very fewer quantity trades being confirmed. Durgapur pellet prices have increased to INR 7,000-7,100/MT against last week at INR 6,900/MT. Offers in Raipur increased to INR 7,200/MT (Ex-plant) against the end of the last week assessment at INR 7,000/MT ex-plant.

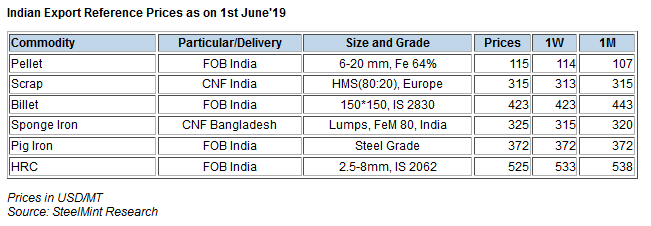

KIOCL(Southern India) had concluded pellet export deal of floated export tender on 30th May, offering 50,000 MT pellet consisting of Fe 64% content with less than 2% Al. As per sources, the deal was concluded at around USD 119/MT, FoB India. SteelMint's assessment for regular grade Fe 64%, 3% Al stands at around USD 124-125/MT, CFR China.

-- SAIL (Steel Authority of India Limited) has announced fiscal year end results for FY19. The company's crude steel output surge by 8% in FY19 to 16.3 MnT as compared to 15 MnT in previous fiscal. Saleable steel production increase by 8% to 15.1 MnT in FY19 as compared to 14.1 MnT in previous fiscal.

COAL

Seaborne premium hard coking coal prices for ex-China markets continue to weaken since the middle of this month. Although Chinese delivered prices for premium HCC have managed to hold firm over the same period. The premium low-volatility segment of the Australian hard coking coal market seemingly appeared to be turning into a buyers' market, amid lacklustre demand showing signs of strain in keeping up with a glut of coking coal supply.

Multiple sources concurred that most buyers in China have been staying away from the seaborne market, citing current price levels above USD 200/MT CFR China for premium materials. In the meantime, however, the second-tier hard coking coal prices have trended upward for much of the previous week on fresh bookings.

Elsewhere in the Indian market, spot demand for Jul-August loading cargoes of imported coking coal has now moderated due to an approaching monsoon.

-- Latest offers for the Premium HCC grade are assessed at around USD 217-218/MT & for the 64 Mid Vol HCC grade at around USD 200/MT CNF India.

SCRAP

Indian imported ferrous scrap market witnessed improved trade activities post election results, while scrap offers inched down slightly on account of recent downtrend observed at global levels after sharp jump last week. Significant buying interest remains subdued amid extreme summer conditions in most of the regions and limited support from end users in the country. Scrap bookings are expected to increase post-Eid-holidays towards Mid-June before Monsoon’s impact to pull down the activities.

-- SteelMint’s assessment for containerised Shredded from Europe and UK stand in the range USD 330-333/MT, CFR Nhava Sheva, slightly down by USD 2-3/MT against last week’s report. Few leading suppliers are offering Shredded at around USD 335/MT, CFR Nhava Sheva and USD 340/MT, CFR Vizag. They were not ready to lower offers further resulting in limited trades.

-- South African HMS 1&2 offers stand in the range of USD 330-335/MT, CFR. Few offers of Dubai HMS 1&2 scrap were heard in the range of USD 325-327/MT as per quality amid limited supply on ongoing Ramadan month. Few trades for West African origin containerised HMS were reported in the range of USD 310-315/MT, CFR India.

SEMI FINISHED

In a week duration, domestic Billet offers fell in the range of INR 100-400/MT (upto USD 6) in major markets. In line sponge iron offers slump by INR 200-400/MT in major markets except in Durgapur east India, over weak demand.

-- Indian Sponge iron export offers to Bangladesh continued rally due to rising prices in Indian market. Latest assessment is at USD 310-315/MT CPT Benapole (dry port of India & Bangladesh), this is equivalent to USD 325-330/MT CNF Chittagong, Bangladesh.

-- Indian induction grade Billet (100*100 mm) export offers to Nepal reported at around USD 445/MT (ex-mill at West Bengal), equivalent to USD 475/MT CFR Nepal (Raxaul border).

-- Punjab State Electricity Commission announces hikes tariff by 2.14% w.e.f 1st Jun'19.

-- SAIL’s Rourkela Steel Plant (RSP) tender held on 22nd May'19 to sell about 3,000 MT steel grade pig iron, had received good response. As per sources, the company had kept base price at INR 27,250/MT, although the material have been fetch high bids of INR 50-100/MT to INR 27,300-27,350/MT ex-plant and total material have been sold.

-- Jindal Steel has raised prices and reported steel grade pig iron at INR 28,200/MT ex-Raigarh & panthers shots(granulated pig iron) at INR 27,000/MT ex-Angul, Odisha.

-- SteelMint's Pig iron export price assessment stood at USD 370-375/MT FoB India, USD 320-322/MT FoB Brazil & USD 332-334/MT FoB Black sea.

FINISH LONG STEEL

Indian Finish long steel market was in positive trend in the beginning of week where prices slightly strong. However by the end of week days, poor demand has narrowed down price range by INR 100-500/MT in Rebars, in which the major slump of INR 500/MT marked in Hyderabad, while remaining markets registered price corrections of INR 100-300/MT through the mid sized mills.

In context to large scale mills, as per conversation with the closed sources with the officials, trades were not up to the mark in May'19, although high cost raw materials are influencing them to keep prices strong. Further as per sources, the mills may slightly increase or roll-over rebar prices for June deliveries in line with tight raw materials.

-- As per assessment, the trade reference Rebar prices (12-25 mm) hovering at INR 35,100-35,300/MT ex-Raipur & INR 36,500-36,700/MT ex-Jalna; prices are excluding of 18% GST.

-- Central region based heavy structure manufacturers offering trade discount of around INR 400-500/MT and current trade reference prices at INR 39,100-39,300/MT (200 Angle) ex-work.

-- Trade discounts in Raipur Wire rod increased further this week at INR 1,300-1,500/MT, which was last week at INR 1,000-1,200/MT. However basic prices steady as against last week closing at INR 37,700/MT ex-Raipur & INR 36,800-37,300/MT ex-Durgapur, for 5.5 mm.

FLAT STEEL

SteelMint got indications that major Indian steel mills may hike Finished Flat steel prices in June by INR 750-1,000/MT owing to increased production cost. However dull automotive demand and limited deals in trade segment remain matter of concern for absorbing this price hike.

Currently HRC (2.5-8 mm, IS2062) prices in traders market is around INR 41,000-41,500/MT ex-Mumbai & INR 40,700-40,800/MT ex-Delhi. And the CRC (0.9 mm,IS 513) prices in traders market is around INR 45,500-46,000/MT ex-Mumbai & INR 45,500/MT ex-Delhi. Prices mentioned above are basic and excluding 18% GST.

Domestic HRC & CRC prices continued to remain under pressure in traders market over sluggish demand since last two months amid General Assembly Elections. If market sources to be believed hike in flat steel prices will be difficult to absorb in domestic market due to poor sales in auto sector and stalled infrastructure projects over delayed funding. Also approaching monsoon season may lead to slowdown in buying activities in domestic market.

However announcement on price revision is still awaited. If cost of production increases then Indian steel mills may consider price hike in the month of June in order to recover the cost.

source: SteelMint

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution