Indian Steel Market Weekly Snapshot

During the week-14 (1st-6th April), Indian spot trades were subdued and due to disruption in power supply in Central region, the prices of Billet & Rebars found support, meanwhile sponge iron prices remained slightly fluctuates on improved availability.

As per SteelMint's assessment, in these days the prices of Sponge iron fluctuated by INR 100-500/MT. However, Billet & Rebar prices surged close to INR 500-1,000/MT (USD 7-14) through the mid sized mills.

In context to price movements through the large mills, they have raised prices this week for both Finished long & flat steel products by INR 500-1,000/MT (USD 7-14) for April deliveries.

Iron ore and Pellets

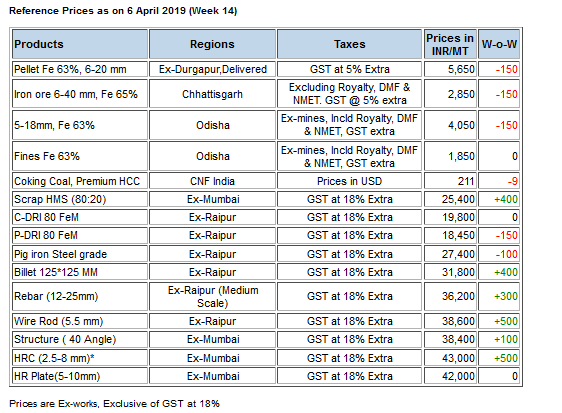

Odisha based merchant iron ore miners decreased iron ore offers by INR 300-400/MT. Odisha Mining Corporation (OMC) has received flat bids and fetched 74% material getting booked at base price. Currently Odisha iron ore trade prices are assessed at INR 4,000-4,100/MT (ex-mines) for 5-18 mm and INR 1,800-2,000/MT (ex-mines) for fines.

Central India, Raipur based pellet manufacturers had reduced offers by INR 200/MT to INR 6,100/MT ex-plant for Fe 63% grade. Southern India, Bellary pellet offers for Fe 63% grade almost stable at INR 6,800-7,000/MT. The prices are excluding GST.

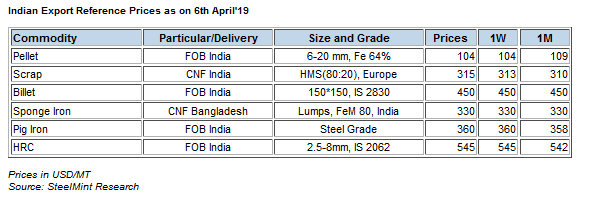

-- Odisha (eastern India) based a pellet maker has concluded two pellet export deals for around 50,000 MT of regular grade pellets (Fe 64%, containing 3% alumina) at around USD 114/MT, CFR China for Apr’19 shipment- Sources.

-- SAIL, India’s govt owned steel mill has reported crude steel production at 16.3 MnT in FY19, up by 8% against 15.02 MnT in previous fiscal.

Coal

Seaborne metallurgical coal spot prices have continued to decline over the past few weeks, following the emergence of lower offers across markets, despite several trades booked and sell tenders concluded recently in China.

Currently, the Chinese traders are buying at FOB price levels of around US$ 200/MT, because seaborne materials are cheaper compared to domestic coals of similar specifications. Meanwhile in Australia, the cyclone season is almost over, and the normalised supply of coking coal available in China is expected to soften prices further.

Latest offers for the Premium HCC grade are assessed at around USD 210.80/MT and for the 64 Mid Vol HCC grade at around USD USD 186.20/MT CNF India.

Scrap

Indian imported scrap market observed slow trades on upcoming elections and less cash inflow. Prices for Shredded scrap corrected marginally while that of Dubai HMS 1 remained almost flat against last week.

SteelMint’s assessment for containerised Shredded from UK, Europe and US stands in the range USD 332-335/MT, CFR Nhava Sheva. HMS 1 from Dubai traded at stable levels of around USD 328-330/MT CFR, while suppliers were quoting in the range USD 330-333/MT, CFR depending on origin. P&S scrap sold at USD 345-347/MT, CFR. West African HMS 1&2 in 20-21 containers traded at USD 305/MT, CFR Mundra and USD 310-313/MT, CFR Goa and Chennai.

Semi Finished

Indian Sponge iron market observed volatility in prices by INR 100-500/MT (USD 1-7) on fluctuating demand & seasonal strengthening supply. However Billet offers rise by INR 400-800/MT(upto USD 12).

-- Punjipatra, Raigarh based steel manufacturers are still facing problems of power cut by JSPL. The plant's are getting power supply of about 12 hrs per day, 50% less than the earlier during Mar'19.

-- Indian sponge iron export offers for 78-80 FeM sponge lumps hovering at USD 310/MT CPT Benapole (dry land port of Bangladesh & India) and USD 330/MT CNF Chittagong, Bangladesh.

-- Indian induction grade Billet (100*100 mm size) export offers to Nepal are reported at USD 455-460/MT (ex-mill at West Bengal), equivalent to USD 485-490/MT CFR Nepal (Raxaul border). Offer rise by USD 5-10/MT W-o-W.

-- Rashtriya Ispat Nigam Limited (RINL) have concluded the tender for the lots comprising of size 77*77 and 65*65 mm (grade IS 2830 Gr A) at around USD 455-458/MT, FoB. Each billet lot offered was of 10,000 MT.

-- MMTC - a leading international trading company in India has invited tender for export of 20,000 MT Billets (150*150 mm). Interested bidders can submit their bids till 09 Apr’19 at 14:30 Hrs

-- RINL has invited tender for export of 10,836 MT Billets to Nepal. Interested bidders can submit their bids till 12 Apr’19 at 11:00 hrs.

-- Private pig iron producers in eastern India have raised prices by INR 200/MT on rising Billet prices & better response. Steel grade prices hovering at INR 27,700-28,000/MT ex-Durgapur & INR 26,400-26,500/MT ex-Jajpur, Odisha.

-- Jindal Steel has maintained offers this week and reported steel grade Pig iron at INR 27,600/MT ex-plant, Raigarh, Central India.

-- MMTC- India’s largest and state-owned trading house, has floated export tender of 30,000 MT non-alloy Pig Iron on behalf of NINL. The due date for submission of bids is 14:30 hrs on 15 Apr’19.

-- Tata Metaliks has reduced Pig iron prices by INR 600-800/MT & offered Foundry grade(2-2.5% Si) at INR 32,500/MT & Low Silicon (1-1.5%) at INR 29,000/MT (USD 420). The prices are ex-plant, Kharagpur, eastern India.

-- SAIL’s Rourkela Steel Plant (RSP) tender held on 3rd Apr'19 to sell about 18,000 MT steel grade pig iron, had received weak response. The base price for the tender was quoted by RSP at INR 26,450/MT (ex-plant) and near about 89% (16,000 MT) material remained unsold.

-- NINL has kept steel grade (N1) Pig iron prices unaltered at INR 26,250-26,650/MT (USD 381-387), ex-Cuttack, Odisha. The company has witnessed 111% surge in its hot metal output for the last financial year ended March 31, 2019 (FY19).

-- SteelMint's Pig iron export price assessment stood at USD 359-361/MT FoB India, USD 339-341/MT FoB Brazil & USD 349-351/MT FoB Black sea.

Finish Long

Indian Finish long steel market remained positive amid sufficient trade volume across regions with rising raw materials. In addition, trade discounts were also limited in Rebar from mid of week onwards.

However, week begins with slight dull sentiments and sudden better response cleared back log up to certain level as prices moved up by around INR 1,000/MT. Meanwhile the participants are assuming that, prices should find stability for near term looking at election season in the country and significant rise in prices.

-- During the week, large mills have increased finish long prices by INR 500-1,000/MT in across regions. Latest offers for 12 mm Rebar is hovering around INR 41,000-41,500/MT, Ex-Mumbai & excluding GST.

-- Medium mills trade reference rebar prices (12-25 mm) assessed at INR 37,700-37,900/MT Ex-Jalna & INR 36,200-36,400/MT Ex- Raipur; prices are basic & excluding GST.

Further, central region based heavy structure manufacturers maintaining trade discount at close to INR 400-600/MT and current trade reference prices at INR 39,500-39,800/MT (200 Angle) ex-work.

-- Blast furnace grade Wire rod offers by Electrosteels Ltd based in Bokaro, Jharkhand heard at close to INR 42,000/MT (ex-plant) for low carbon & 5.5-6.0 mm.

Flat Steel

Major Indian steel mills announced hike in flat steel prices in the beginning of the week by INR 500/MT (USD 7) for April deliveries. Following the suit, govt owned - SAIL has also raised domestic HRC & CRC prices by around INR 500-1,000/MT (USD 7-15) for April deliveries. After increase, company’s effective prices for HRC (2.5-8 mm, IS 2062) is around INR 43,250/MT ex-Mumbai. Meanwhile CRC prices surge by INR 1,000/MT in April. Thus after increase revised offers for CRC (0.9 mm, IS513Gr) is INR 48,500/MT ex-Mumbai.

After increase JSW Steel’s effective price of HRC (2.5-8 mm, IS2062) is in range of INR 43,000-43,250/MT ex-Mumbai. Meanwhile revised offers of Essar Steel is at INR 43,250/MT ex-Mumbai.

However increased prices have not yet passed on to the traders market for April deliveries.

Indian steel mills have raised domestic HRC prices following hike in imported HRC offers from major exporting nations like Japan and Korea. As per sources, annual maintenance is planned at Tata Steel’s Jamshedpur plant and Bhushan Steel, which will keep supply tight in near term and may push prices in domestic market.

source: SteelMint

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution