Iron Ore Prices Seen Stagnant on Rising Supplies, Asia Demand to Support

New Delhi – Global iron ore prices are seen stagnating in the next few years on excessive supplies and slowing Chinese demand, yet a strong growth elsewhere in Asia is expected to keep prices supported and trade booming.

The trigger for price falls has come from the largest steel producer China that is facing a slower economic growth and is modernizing its industry to cut pollution. Large stocks of steel scrap available for recycling is also damping the outlook for iron ore.

However, the second largest steel producer – India -- where a spate of M&As has brought large metal producers to shore, is promising large-scale expansion of steel capacities and as a result, a rising appetite for iron ore.

“In India, the supply-demand situation may remain pretty tight. But otherwise, globally, supply is copious so prices won’t be affected,” said Amit Dixit, associate vice president at Edelweiss Financial Services.

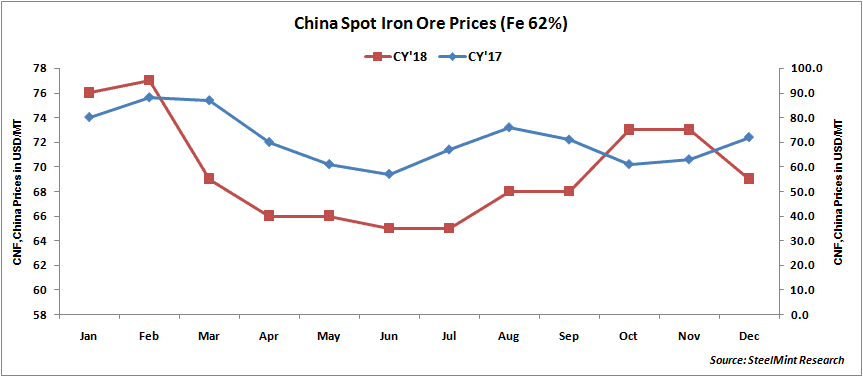

According to Edelweiss, global iron ore is seen at $65 a tonne (62% iron content, FOB) in 2019, a notch down from $66.1/ tonne in 2018.

The company sees the downward pressure continuing, resulting in a dip to $62/tonne in 2020.

“Few years ago, new mines came up in Australia and Brazil which are now working at optimum capacity,” said Hitesh Avachat, group head – corporate ratings at Care Ratings Ltd. “So, iron ore production is matching the rise in demand from the steel sector.”

Like Dixit, Avachat also predicted nearly similar prices of iron ore this year. Avachat said average global prices are unlikely to fall below $60/tonne. He attributed the US shutdown and uncertainty on account of upcoming Indian general elections to have prompted the recent plunge in iron ore prices.

The World Steel Association has forecast that the global steel production will rise by 1.4% to reach 1,681.2 million tones this year. In India and other Asian countries, the growth is expected to be much higher.

source: SteelMint

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution

Henan Jiyuan Iron & Steel awards Danieli for new Jumbo Rounds caster in China