Homecoming costs tycoon $7B in year of legal drama

It’s been a tough year as India’s fourth-richest man has struggled to return to his roots.

When Lakshmi Mittal, 68, left India for a vacation through Asia more than four decades ago, he didn’t plan to stay in Indonesia and lay the foundation for a steel empire that spans the globe and generated $5 billion in profits last year. Yet that’s what he did, even as a string of efforts to establish himself in India’s steel market failed — until now.

Mittal’s global giant ArcelorMittal is finally nearing the end of a yearlong battle to break into India with the $5.9 billion acquisition of Essar Steel India Ltd. The Indian steelmaker was put on the block after its lenders approached the court to recover about $7 billion in dues.

The forced sale of the 10 million metric tons a year mill has hit numerous roadblocks including rules that compelled Mittal to shell out an extra $1 billion to clear the dues of two firms where he held some stake and to reportedly sell his holdings in one of them for 1 rupee a share.

We have acquired lots of companies around the world. For the first time, we have been sued for acquiring a company

Perhaps the biggest hurdle was posed by Essar Group’s Ruia brothers, who lost control of the mill after a regulator pushed it into bankruptcy court. Challenges from Essar Group, rival bidders and some creditors have seen ArcelorMittal make dozens of trips to court since an initial bid in February 2018 — dwarfing its five-month long campaign for Arcelor SA in what was the industry’s biggest merger.

“We have acquired lots of companies around the world. For the first time, we have been sued for acquiring a company,” Aditya Mittal, Mittal’s 43-year-old son and the company’s chief financial officer, said in a BloombergQuint interview in January. “These are unique circumstances.”

The legal wrangling landed in the Supreme Court last year, setting precedents for India’s two-year-old bankruptcy law. The drama also sounded a warning to other founders, who till recently were accustomed to an ineffectual court system and to walking away from debts without serious consequences.

Starting out

Lakshmi Mittal, named for the Hindu Goddess of prosperity, was born in a village in India’s northwestern state of Rajasthan, where, he has said, a lack of electricity and water made his early years difficult. Mittal joined his father’s steel business early and went on to set up Mittal Steel Co. in 1976 in Indonesia, before spreading out to Trinidad, Mexico and Germany. In 1994 the family business was split.

Mittal’s initial success overseas helped him decide that his future lay outside India, he has said, and he also wanted to avoid conflicts around expansion plans within the family.

Brothers Pramod and Vinod Mittal eventually sold their debt-laden local steel business, while ArcelorMittal gained a foothold in India through a minority investment in processed steel producer Uttam Galva Steels Ltd., which was ultimately sold. Mittal also took a 49 percent stake in a local oil refinery through a family investment company in 2007.

Mittal’s India Steel Forays Mittal’s efforts to establish itself in India predate the 2006 merger with Arcelor. The steelmaker signed an agreement to set up a plant in Jharkhand in 2005 and one in Odisha in 2006. It ditched the Odisha project in 2013 after failing to get permits for land and iron ore mining. Plans for the Jharkhand venture and another in Karnataka weren’t successful. The steelmaker tied up with the state-run Steel Authority of India Ltd. in 2015. The two companies haven’t yet signed the final terms for a 60 billion rupee plant to cater to the automobile sector.

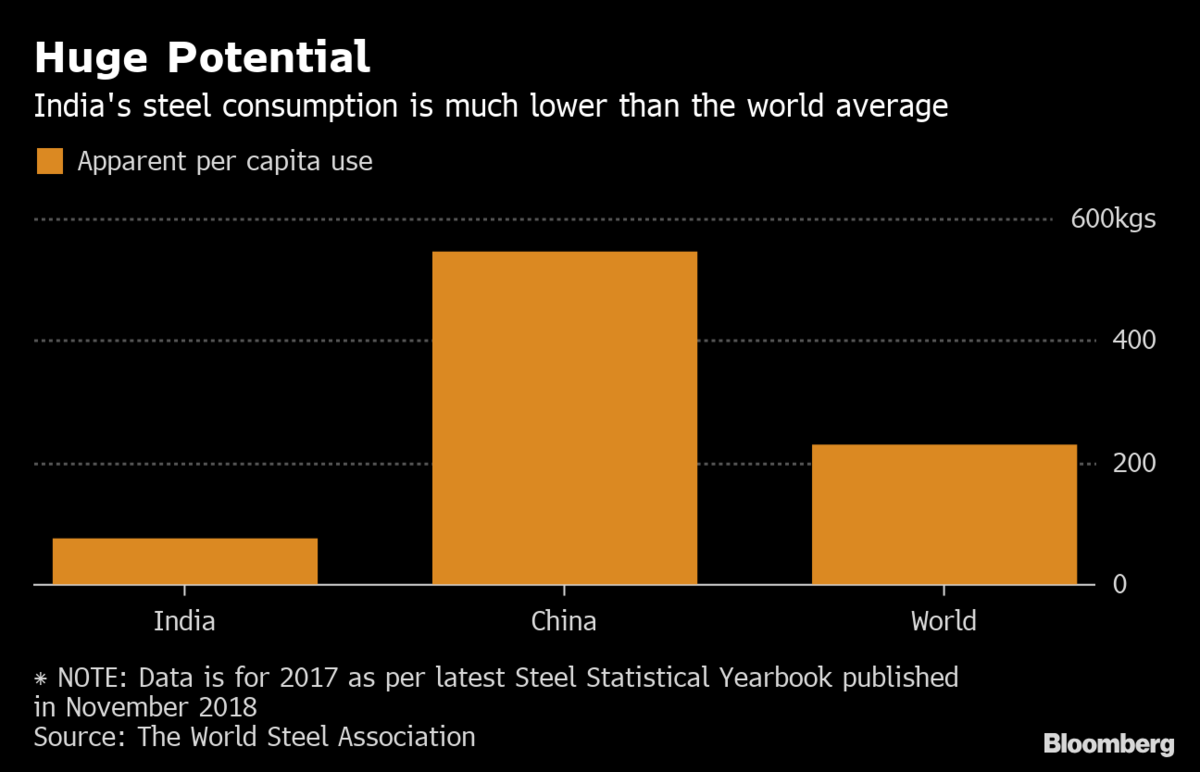

Essar Steel’s capacity will immediately make ArcelorMittal the fourth-biggest player in a nation where the administration plans to invest trillions of rupees in infrastructure. The government has a mandate to use locally-produced steel for projects under the “Make in India” campaign and has in the past curbed overseas inflows with minimum import price limits and anti-dumping taxes.

ArcelorMittal is partnering with Nippon Steel & Sumitomo Metal Corp. for the purchase, though it will hold a controlling stake.

ArcelorMittal has a strong market position globally in the automobile sector, and its entry in India may give more options to domestic auto majors

“India is very focused on developing its own industrial backbone,” Aditya Mittal said in February after ArcelorMittal’s quarterly earnings. “The growth that exists in India is not really a growth that is available to imports, but primarily to domestic players.”

The acquisition would increase competition in India’s already concentrated flat steel category, according to Jayanta Roy, a senior vice president at ICRA Ltd., the local arm of Moody’s Investors Service. “ArcelorMittal has a strong market position globally in the automobile sector, and its entry in India may give more options to domestic auto majors.”

Without doubt India’s insolvency process is reshaping its steel industry. Five companies from the sector were among 12 large debtors — the so-called dirty dozen — ordered into bankruptcy court in 2017 by the regulator in a clean-up of one of the world’s worst piles of bad debt. Those cases are, in turn, impacting the law.

Five months after the regulator’s order, the government intervened to ban what it called “habitually non-compliant” people from using the bankruptcy process to regain control of their delinquent companies with reduced debt burdens.

The change hit the Essar Steel sale when bidders ArcelorMittal and VTB Capital-led Numetal Ltd. were disqualified for links to non-performing companies. ArcelorMittal’s offer was invalidated because of the outstanding dues of two non-performing group companies, while Numetal’s was rejected as one of its investors was the son of an Essar founder.

ArcelorMittal eventually cleared the dues in question after sweetening its bid, which the Ruias then topped in a last-minute effort to thwart Mittal.

The offers and counteroffers fueled a prolonged legal battle between ArcelorMittal and Numetal, and subsequently the Ruias, prompting the Supreme Court to tighten deadlines mandated by the bankruptcy law and reiterate rules for founders bidding for their delinquent assets.

On Friday, victory for Mittal looked close after a bankruptcy court approved ArcelorMittal and partner Nippon Steel’s offer for Essar Steel. Lenders can expect to recover about 85 percent of dues based on the resolution proposed, estimated Sunidhi Securities Institutional Research, which said the order — unless contested by the previous mill owners — clears the way for an entry by the steel giant into Indian markets.

The Ruias’ Essar Group said Friday that its $7.8 billion offer remained “the most compelling” and on Monday approached a higher appeals court against the approval for the ArcelorMittal takeover. That follows a plea by Standard Chartered Plc, the third-biggest lender to the mill, in the same appeals court opposing the approval of ArcelorMittal’s plan as a substantial part of its dues will remain unpaid, according to people with knowledge of the matter.

source: MINING.COM

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution

Henan Jiyuan Iron & Steel awards Danieli for new Jumbo Rounds caster in China