Analysis: China's rising steel output in balance with domestic property demand

China's apparent consumption of crude steel over January-July rose 8.9% on year to 526.76 million mt and will be robust enough to absorb the surge in domestic steel production this year, according to S&P Global Platts estimates.

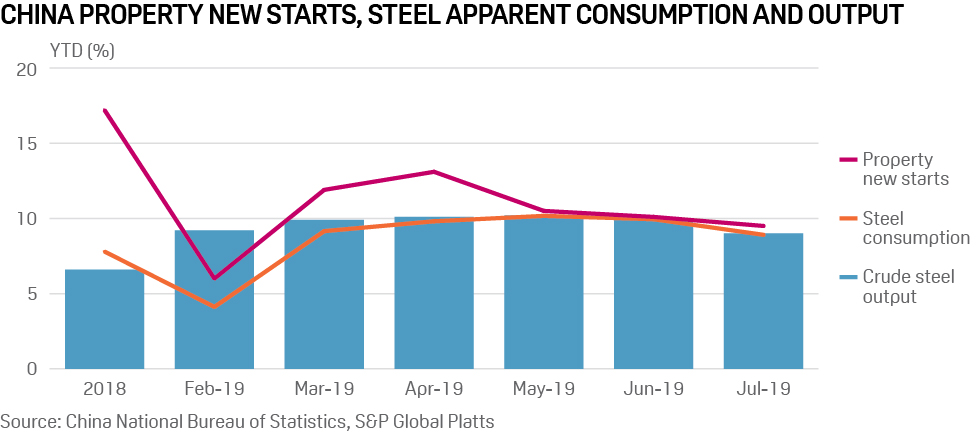

The consumption growth rate grew in tandem with new property construction starts, suggesting that strong domestic demand was the core driver behind soaring steel output this year.

China's loosening of environmental protection constraints on production, along with steel capacity expansion, have also contributed to steel output rising by around 10% to date in 2019.

Property construction accounts for more than 30% of Chinese steel consumption and is the biggest driver of steel demand. The sector is expected to slow over the remainder of 2019 -- but so will the growth rate of crude steel production.

As a result, steel supply and demand will remain in balance, while mill profit margins will retreat in relation to the high levels seen in 2018. Iron ore prices have also corrected to below $90/mt CFR after touching a five-year high of $126/mt in July, which will also help steel margins.

A slower growth rate of new property starts in 2019 is in line with market expectations, after land purchases and home sales decreased by 29.4% and 1.3% on year respectively over January-July 2018. However, the slower growth rate of new housing starts is not expected to adversely impact demand for steel -- although it may seem weaker compared with last year, 2018 was particularly strong.

The decline in land purchase and home sales is mainly because demand from home buyers had been pulled forward to 2015-2018 because of Beijing's monetary and fiscal stimulus measures.

On the supply side, the yearly growth rate of China's crude steel production over January-July decelerated to 9% from a peak of 10.2% over January-May. The dip in production was due mainly due to strengthened output cuts in a bid to improve the air quality in northern China over June and July.

Production rates will also be lowered in the run-up to China's National Day on October 1, which this year will be more important than ever as it will mark the 70th anniversary of the People's Republic of China. Local governments in northern China will be told to reduce industrial activity, including steel production, to ensure blue skies over Beijing on the landmark occasion.

China's steel output in 2019 has been catching up with strong steel demand from the property sector, rather than exceeding it. In fact, the pace of steel demand outstripped supply in 2018, as property new starts increased by 17.2% while crude steel rose 6.6% on year. This resulted in rebar profit margins averaging at a very healthy $132/mt in 2018, according to Platts analysis.

The average rebar profit margin to date in 2019 is $67/mt as supply and demand have rebalanced.

China's July crude steel and pig iron output stood at 85.22 million mt and 68.31 million mt respectively, up 5% and 0.6% on year, data released by the National Bureau of Statistics on August 14 showed. China's pig iron output over January-July increased 6.7% on year to 473.44 million mt, the data showed.

source: S&P Global

Related News

Top News

Danieli’s scrap-recycling technology is reaffirmed by Novelis as a trusted solution